Case Details

Case: M/S Rakesh Plastic Furniture & Crockery Emporium v. State of U.P. & Others

Citation: Writ Tax No. 123 of 2021 (Allahabad High Court)

Court/Bench: High Court of Judicature at Allahabad, Court No. 7

Coram: Hon’ble Piyush Agrawal, J.

Date of Decision: 01-09-2025

Issue

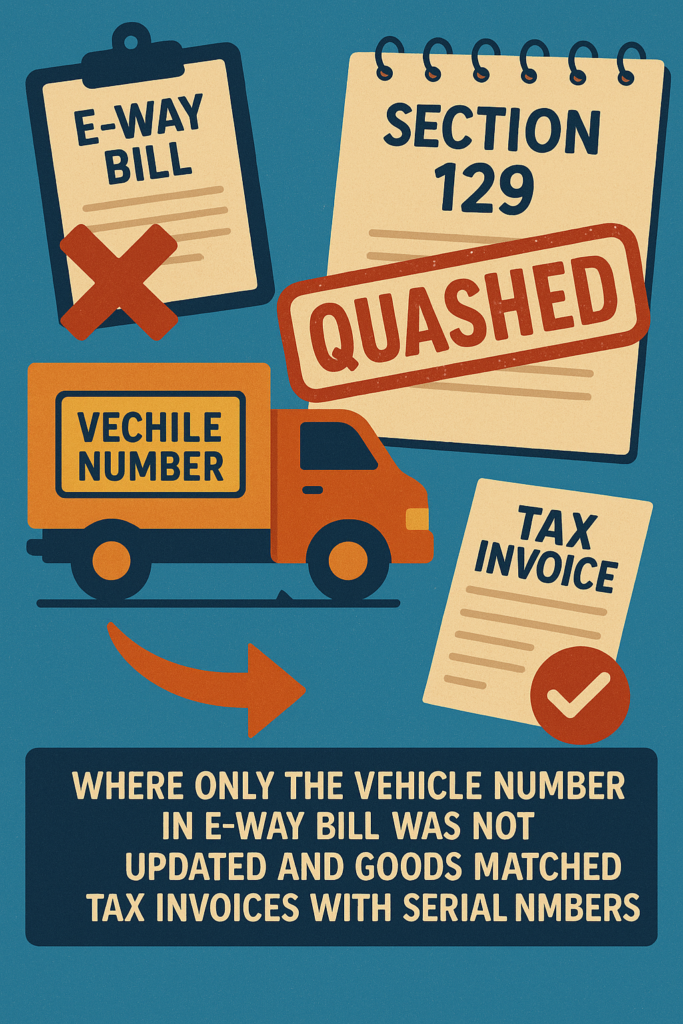

Whether mere non-updation of vehicle number in the e-way bill, absent any discrepancy in goods or documents, justifies detention and penalty under Section 129(3) of the GST law.

Facts

Petitioner purchased branded electronics from an authorised dealer; e-way bills were valid and invoices bore serial numbers.

Due to vehicle defects, the transporter changed the vehicle but did not update the e-way bill.

Goods were intercepted; physical verification found documents correct and items tallying with serial numbers in invoices.

Authority imposed tax and penalty; appellate order upheld the levy; petitioner sought quashing and refund.

Held

It was held that when goods correspond with tax invoices and serial numbers, mere technical breach of not updating the vehicle number in the e-way bill cannot, by itself, establish intent to evade tax. Orders of seizure and penalty were quashed; any amount deposited was directed to be refunded.

Ratio / Key Principle

Technical lapses in e-way bill particulars, without discrepancy in goods or evidence of evasion, do not sustain proceedings under Section 129.

Suggestion for Professionals / Businesses

Ensure transporters promptly update e-way bills on vehicle change and retain evidence of genuine logistical exigencies. Maintain item-level identifiers (e.g., serial numbers) on invoices and transport documents to substantiate compliance during interception and avoid unwarranted penalties.